Canada’s $33 Billion Miscalculation: Betting on the Wrong Battery Chemistry

How Canada’s Industrial Strategy Overlooked the LFP Revolution

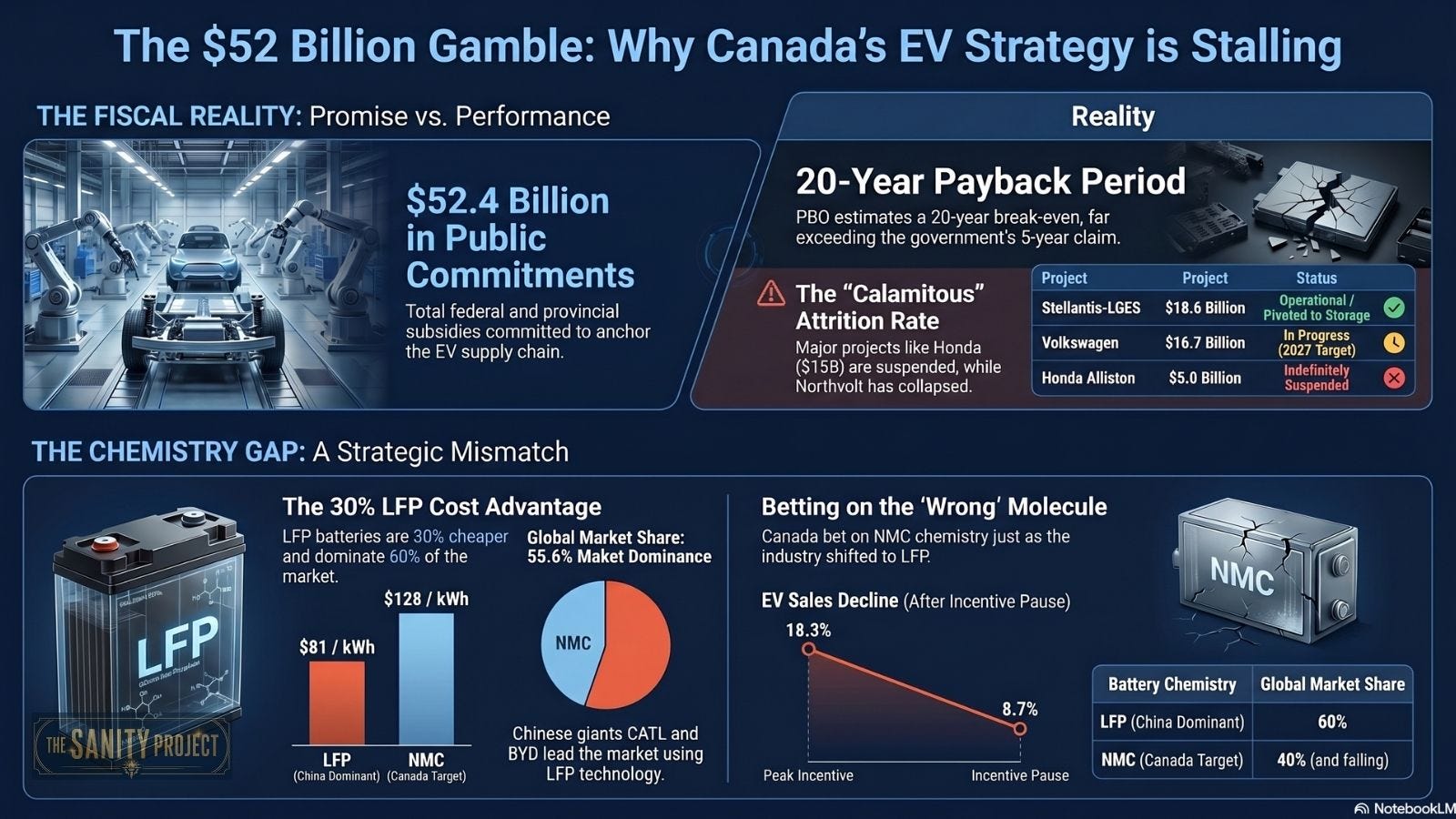

In recent years, Canada boldly committed $33 billion to transform itself into a North American electric vehicle (EV) powerhouse. The strategy hinged on battery manufacturing, extensive public funding, and promises of economic revitalization. But beneath high-profile headlines about tariffs and consumer demand, a more fundamental miscalculation doomed the effort: Canada invested billions in nickel, manganese, cobalt (NMC) battery technology just as the world embraced lithium iron phosphate (LFP) chemistry.

The Heart of the Mistake: Chemistry Dictates Economics

The Battery Wars: NMC vs. LFP

Global automakers have long faced a crucial choice: which battery chemistry to stake their futures on. In the West, companies like Honda, General Motors, and Ford chose NMC for its higher energy density and superior range—key selling points for drivers navigating vast Canadian and American landscapes.

But China bet big on LFP. This chemistry, built from iron and phosphate, avoids costly and volatile minerals like cobalt and nickel. It’s cheaper, safer, and the materials are far more abundant. The trade-off was historically range—iron is heavier, LFP batteries were bulkier, and Western automakers feared range anxiety would ruin market appeal.

China Out-Engineers the Range Problem

Chinese innovators didn’t accept these limits. Companies like BYD pioneered engineering breakthroughs—most notably the “blade battery”—which transformed how LFP cells are packed into cars. By eliminating heavy protective modules and integrating the batteries into the car’s structure, they eliminated much of LFP’s range disadvantage.

Suddenly, LFP wasn’t just cheaper; it was viable for mainstream vehicles. As a result, LFP now dominates 81.5% of China’s domestic battery market and about 60% of the global market.

The Permanent Financial Gap

The economic consequences of Canada’s bet became clear through hard numbers. Building an EV battery with NMC chemistry is structurally more expensive due to the scarcity and higher cost of its materials. For a standard 60 kWh battery pack, NMC can cost $2,820 more per vehicle than LFP. Multiply this cost across hundreds of thousands of vehicles, and the result is a multi-hundred-million-dollar annual disadvantage.

Importantly, this isn’t just a cyclical issue—it’s embedded in molecular reality. Nickel and cobalt will always be pricier, so no amount of policy tweaking or tariffs can close that gap. This permanent disadvantage is what led Honda to suspend its $15 billion Ontario battery plant and raises existential questions about the future of other planned facilities.

Policy Anchored to the Wrong Resource

Canada’s strategy didn’t just rely on manufacturing; it also focused on domestic mining, touting nickel and cobalt as key national assets. But in a market rapidly tilting toward LFP, these minerals lost their relevance. Billions were spent subsidizing factories dependent on a battery technology most of the world was already leaving behind. Even if NMC had remained relevant, Canadian mine development typically faces 18-year delays—far too slow to keep pace with global innovation.

Looking Ahead: What Does This Mean for Canada?

As the dust settles, the narrative of tariffs and short-term demand crashes is overshadowed by a deeper technological reality. Canada’s heavy subsidy approach set it up for a future that never materialized. With LFP dominance entrenched, only a game-changing leap—such as mass-market solid-state batteries—could give Western automakers a fighting chance.

But that leap is years away. Until then, facilities built on the NMC model face daunting structural headwinds, and key questions linger: Will other major battery plants become stranded investments? Can Canada pivot quickly enough to new battery chemistries, or will it keep matching industrial ghosts?

Conclusion

Canada’s $33 billion EV battery gamble reveals the dangers of industrial policy caught flat-footed by technological change. As LFP chemistry redefines the global market, the lesson is clear: chemistry isn’t just science—it’s destiny in the economics of clean tech.

For the in-depth report, go to our News Site @

https://blog.thesanity.org

Check out our Free White Paper:

For the in-depth report, go to our News Site @ https://blog.thesanity.org